COVID-19 Crisis Market Updates

The methodology used in the COVID-19 analysis is based upon methods discussed in Valuation and Risk Management in Energy Markets, Glen Swindle (Cambridge University Press, 2014). Weather variables, drift and seasonal components represented as Fourier terms are estimated, with variables retained selected by an out-of-sample estimation criterion. Regressions are performed at the delivery bucket level (e.g. 5×16 for peak). The resulting residuals are then corrected for biases resulting from short time-scale effects to account for notable holiday periods.

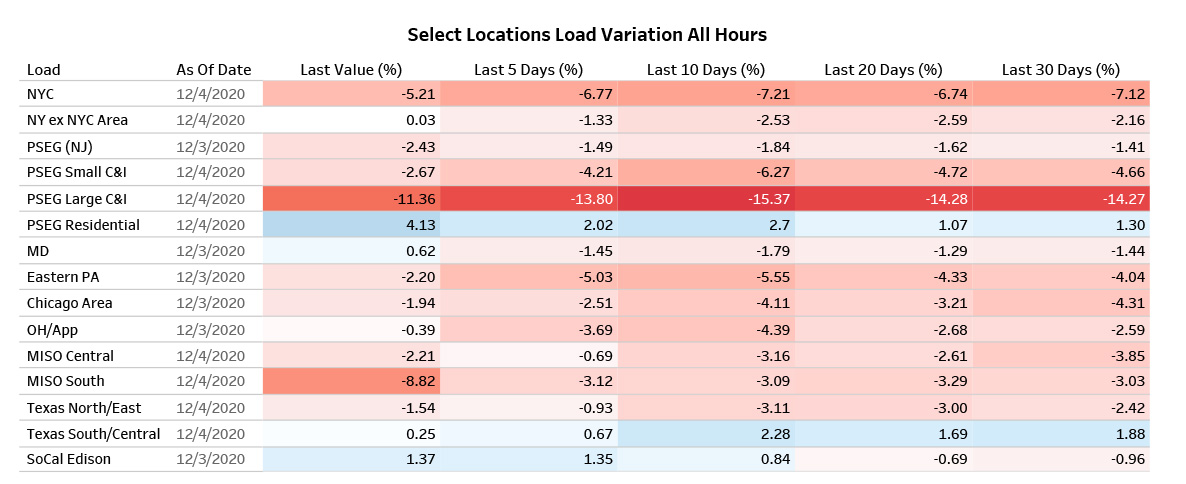

This update on electricity demand destruction uses data available as of the time of reporting. All results are derived from hourly historical demand as published by the market administrators (NYISO, PJM, MISO, ERCOT and CAISO) and are weather-normalized and de-trended. The demand destruction statistics reported here are in percentage departure from normal given prevailing weather conditions and time-of-year.

Full Reports